A private health inquiry process is the structured sequence of steps Canadians follow to obtain private medical assessments, secure insurance authorization, and protect their personal health information under regulated privacy standards. The process covers everything from your first call to an insurer through specialist consultations, diagnostic testing, and final treatment booking. Getting the order right matters. Skipping a single step, like booking a specialist before receiving pre-authorization, can result in a full claim rejection and unexpected out-of-pocket costs. Understanding the private health inquiry meaning before you start saves money, time, and frustration. Tools like Healthnavigatorai help Canadians clarify their symptoms and understand their next steps before entering this process.

What is a private health inquiry process, step by step?

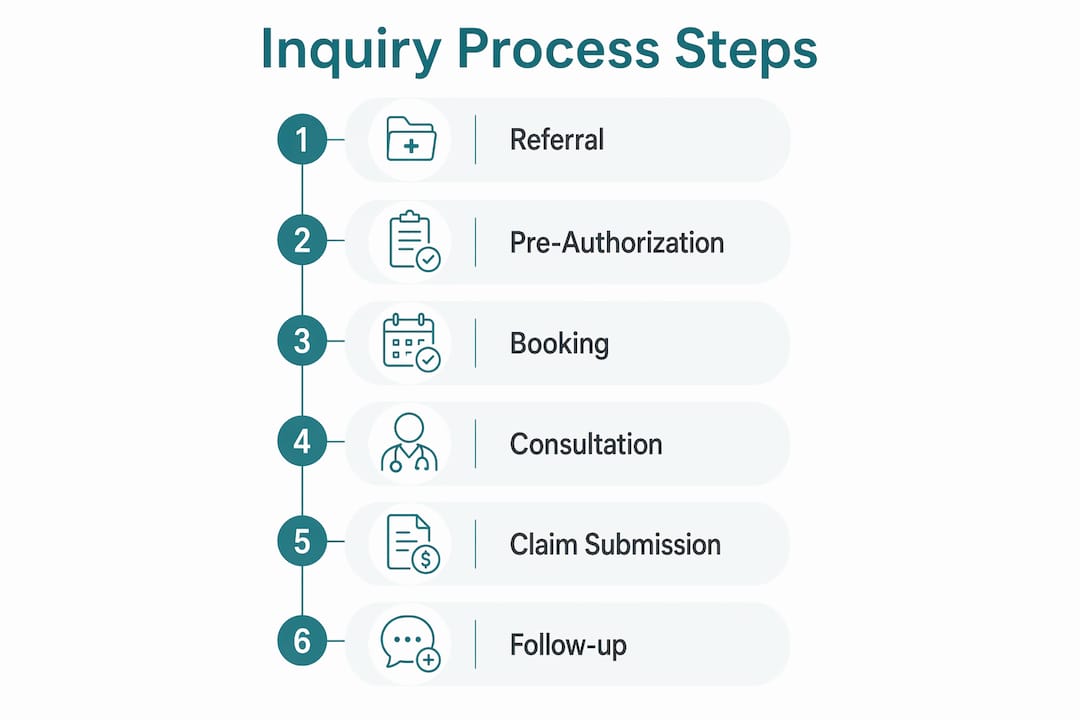

The private health inquiry process follows a 6-step pathway: initial inquiry, GP referral, insurance pre-authorization, specialist consultation, diagnostic testing, and treatment booking. Each step must happen in that exact order. Jumping ahead causes administrative failures that insurers are not obligated to reverse.

Here is what each stage requires:

- Initial inquiry. Contact your private insurer to confirm your policy covers the condition or symptom you are experiencing. Ask specifically about coverage limits, excess amounts, and which providers are recognized under your plan.

2. GP referral. Obtain a referral letter from a clinician recognized by your insurer. Referral letters function as clinical justification of need for specialist or diagnostic services. The referral does not have to come from your family doctor, but it must come from an insurer-recognized clinician to validate your claim.

3. Insurance pre-authorization. Submit the referral to your insurer and request a pre-authorization reference number before booking anything. This is the most commonly skipped step and the most costly mistake.

4. Specialist consultation. Book your appointment only after receiving written authorization. Bring your reference number to the appointment and confirm the specialist's billing code matches what your insurer approved.

5. Diagnostic testing. If the specialist orders tests, each test category (imaging, bloodwork, pathology) may require a separate authorization. Confirm this with your insurer before the tests are performed.

6. Treatment booking. Once diagnostics are complete and a treatment plan is established, request final authorization for the procedure. Ask for an itemized quote and verify it includes all fees, since private treatment quotes sometimes exclude complication fees or post-care costs.

Pro Tip: Write down your pre-authorization reference number and the name of the insurer representative who issued it. If a claim dispute arises later, that record is your strongest evidence.

Following the correct administrative order is the single most reliable way to avoid claim rejection. Patients who book appointments before authorization face 100% claim rejection with no recourse from the insurer.

How is patient confidentiality maintained during private health inquiries?

Protected health information (PHI) refers to any data that identifies a patient and relates to their health condition, treatment, or payment. Federal privacy rules establish patient rights over their health information and limit third-party access. In Canada, the Personal Information Protection and Electronic Documents Act (PIPEDA) governs how private health data is collected, used, and disclosed. Understanding your rights under PIPEDA rules is the foundation of any private health inquiry.

Clinical best practices reinforce these legal protections during actual consultations. The AIDET mnemonic (Acknowledge, Introduce, Duration, Explanation, Thank You) is a clinical communication standard used during health assessments to build rapport and protect patient privacy. It structures the interaction so patients feel safe sharing sensitive information without fear of unnecessary disclosure.

Key privacy safeguards you should expect during a private health assessment:

- Consent before disclosure. Your insurer or clinician must obtain your written consent before sharing your health data with any third party, including other providers.

- Minimum necessary standard. Clinicians and insurers share only the health information required for the specific purpose, not your full medical history.

- Anonymized health searches. When researching symptoms or conditions online before your inquiry, use platforms that do not require sign-up or store personal data. Healthnavigatorai offers anonymous health search options designed for Canadians.

- Secure document handling. Any medical documents you submit to an insurer or clinic should travel through encrypted channels. Avoid sending health records by unencrypted email.

- Right to access your records. You have the right to request copies of any reports generated about you during the inquiry process, including insurer-commissioned medical assessments.

Pro Tip: Before your first consultation, ask the clinic directly: "Who will have access to my records, and how are they stored?" A reputable private provider answers this question without hesitation.

Health inquiry consultations also rely on active listening techniques to encourage patients to share subjective and emotional health data. That information is clinically valuable and equally protected under privacy law.

What challenges arise with pre-existing conditions and insurer assessments?

Pre-existing condition disputes are among the most common reasons private health claims are denied in Canada. Insurers use fund-appointed medical practitioners to assess whether a condition existed before the policy start date. Patients rarely realize they can request copies of these assessment reports, and that oversight is costly.

The insurer's medical practitioner report is the document that drives the denial decision. Without reading it, you cannot build a targeted counter-argument. Once you have the report, the most effective response is a detailed letter from your treating GP or specialist that addresses the insurer's specific assessment points directly.

Common challenges during this phase include:

- Vague denial letters. Insurers sometimes issue denials without specifying which clinical finding triggered the pre-existing condition ruling. Request the full assessment report in writing.

- Disputed timelines. Insurers may claim a condition existed before your policy start date based on incomplete records. Your treating doctor can provide a clinical timeline that contradicts this.

- Lack of clinical evidence on file. If your GP has not documented your condition thoroughly, the insurer's version of events carries more weight. Ask your doctor to write a detailed clinical letter addressing the insurer's exact claims.

- Missed complaint deadlines. Regulated markets require insurers to acknowledge complaints within 2 business days and respond substantively within 10 business days. Missing your window to escalate forfeits your right to a formal review.

> "The key to overturning a pre-existing condition denial is clinical evidence that directly addresses the insurer's specific assessment points, not a general letter of support from your doctor."

Pre-existing condition disputes can be successfully challenged when patients provide detailed, targeted evidence from their treating physicians. General letters of support rarely succeed. Specificity wins.

How can you navigate insurance authorization requirements effectively?

Pre-authorization is not a formality. It is the administrative gate that determines whether your insurer pays or you do. Booking before authorization causes claim rejections and out-of-pocket expenses that the insurer has no obligation to cover retroactively.

Insurers issue separate authorizations for consultations, diagnostics, and treatments. Each one requires its own confirmation. That means a single episode of care can require three separate authorization requests. Tracking each one in writing prevents gaps.

| Authorization type | What it covers | What to confirm |

|---|---|---|

| Consultation | Initial specialist visit | Provider recognition, referral validity |

| Diagnostics | Imaging, bloodwork, pathology | Each test category separately |

| Treatment | Procedure or surgery | Itemized quote, facility recognition |

Provider eligibility is a separate check from authorization. A specialist can be licensed and reputable but not recognized by your specific insurer. Always confirm provider recognition before booking. Ask your insurer for a list of recognized providers in your region or verify through specialist booking tools that cross-reference coverage.

Coverage limits and excess amounts also affect authorization decisions. If your policy has a $500 excess, you pay that amount before the insurer contributes. If your coverage limit for physiotherapy is $1,000 annually and you have already used $800, your remaining authorization will reflect only $200. Know your remaining balance before each authorization request.

Pro Tip: Keep a dedicated folder (physical or digital) for every authorization reference number, approval letter, and insurer contact name. If a claim is disputed months later, this folder is your complete paper trail.

Key Takeaways

A private health inquiry process requires strict adherence to the correct administrative sequence: referral, then pre-authorization, then booking, with privacy protections and documented evidence at every stage.

| Point | Details |

|---|---|

| Follow the 6-step sequence | Skipping pre-authorization before booking causes full claim rejection with no insurer recourse. |

| Know your privacy rights | PIPEDA governs your health data in Canada; you can request copies of all reports generated about you. |

| Challenge denials with specifics | A targeted letter from your treating doctor addressing the insurer's exact findings overturns more denials than general support letters. |

| Track every authorization separately | Consultations, diagnostics, and treatments each require their own insurer authorization and confirmation. |

| Use privacy-first tools | Platforms like Healthnavigatorai let you assess symptoms and upload documents without storing or selling your data. |

What I've learned from watching Canadians navigate private health inquiries

The most common mistake I see is not ignorance of the process. It is overconfidence in the insurer's goodwill. Patients assume that if they have valid coverage and a legitimate medical need, the claim will be paid. That assumption costs them.

The administrative order is not bureaucratic red tape. It is the legal framework that defines whether your insurer is obligated to pay. A referral submitted after a specialist appointment is not a referral for insurance purposes. It is a document that arrived too late. Insurers know this, and they apply the rules consistently.

What actually works is treating the private health inquiry process like a paper trail exercise from day one. Every phone call gets a follow-up email. Every authorization gets a reference number. Every denial gets a formal written response within the complaint window. Patients who document everything win disputes at a far higher rate than those who rely on verbal assurances.

Privacy is the other area where I see Canadians underestimate their rights. You are entitled to see every report an insurer commissions about your health. Requesting that report is not aggressive or unusual. It is your legal right under Canadian privacy law, and it is the only way to build a targeted counter-argument when a claim is denied.

The private health inquiry process rewards preparation. Patients who understand personal health information protections before they start are the ones who get their claims paid and their privacy respected.

> — Rishi

Healthnavigatorai: plain-language support for your health inquiry

Healthnavigatorai is a free, no-sign-up tool built specifically for Canadians who need clear guidance before and during a private health inquiry. It does not sell or share your data.

You can check your symptoms in plain language and receive an immediate assessment that tells you which type of specialist to seek and what average wait times look like in your region. If you already have medical documents, the document upload tool lets you submit them securely for a plain-English summary of what they mean and what your next step should be. Both tools are designed to help you enter the private health inquiry process informed, not guessing.

FAQ

What is a private health inquiry process?

A private health inquiry process is the structured series of steps a patient follows to obtain private medical assessments, secure insurance authorization, and protect personal health data under regulated privacy standards. The process typically includes six stages: initial inquiry, GP referral, pre-authorization, specialist consultation, diagnostics, and treatment booking.

What does pre-authorization mean in a private health inquiry?

Pre-authorization is written approval from your insurer before you book any appointment, test, or procedure. Booking without it causes full claim rejection and leaves you responsible for the full cost.

How does PIPEDA protect my health information during a private inquiry?

PIPEDA requires that any organization collecting your health data in Canada obtain your consent, use only the minimum information necessary, and give you access to your own records on request. It applies to private insurers, clinics, and any third party handling your health data.

Can I challenge a claim denial based on a pre-existing condition?

Yes. Request a copy of the insurer's medical practitioner report, then ask your treating GP or specialist to write a letter that directly addresses the insurer's specific clinical findings. Targeted clinical evidence overturns pre-existing condition denials far more reliably than general letters of support.

How long does an insurer have to respond to a health insurance complaint?

Regulated insurers must acknowledge a complaint within 2 business days and provide a substantive response within 10 business days. Missing the escalation window after that response can forfeit your right to a formal review.